Breaking into Fintech: The Spending Intelligence War — A Coupang Case Study by James Briggs

The percentage of South Koreans who feel financially prepared for retirement. The lowest of any country surveyed globally — against a 34% average.

South Korea is one of the most digitally sophisticated financial markets on earth. Digital wallet penetration approaches 98%. Cash accounts for roughly 7% of point-of-sale transactions. Daily simple-payment volume has crossed 1.1 trillion won. Tap, scan, send, done.

Beneath that frictionless surface, a crisis is compounding. More than 60% of Koreans in their 40s and 50s say they are not prepared for old age, even as over 90% recognize the need. Half haven’t started preparing at all.

The structural reasons run deep. Koreans hope to retire at 65 but are actually forced to leave their primary careers around 53–56 — over a nine-year gap between expectation and reality. The barrier cited most often, by more than 60% of respondents, is simply insufficient income. Household debt sits at 186.5% of disposable income, among the highest in the OECD. Young Koreans in their 20s and 30s carry an average of 16 million won in debt on salaries of 37–41 million won. The old-age poverty rate for those 66 and older is 40% — again, the highest in the OECD.

And there are costs that standard retirement planning fails to account for: children’s education averaging 46 million won per child, marriage support averaging 136 million won, medical costs for those over 65 now exceeding 5 million won per person annually — climbing 13% in four years.

Korea solved the convenience of money. It hasn’t solved the security of it. And the company with the deepest understanding of how 23 million Koreans spend might be uniquely positioned to help them start building.

An independent strategic product exercise built entirely on publicly available research — not an official recommendation, internal roadmap, or insider analysis. It explores how a commerce ecosystem like Coupang could move beyond payments into spending intelligence and financial wellness, and it’s meant to show how I think through ambiguous 0-to-1 product problems.

Korea’s wallet war is already won — Toss, Kakao Pay, and Naver Pay locked it up years ago. But the spending-intelligence war hasn’t started. The more defensible entry for Coupang may be commerce-first finance, not a “Toss inside Coupang” super-app.

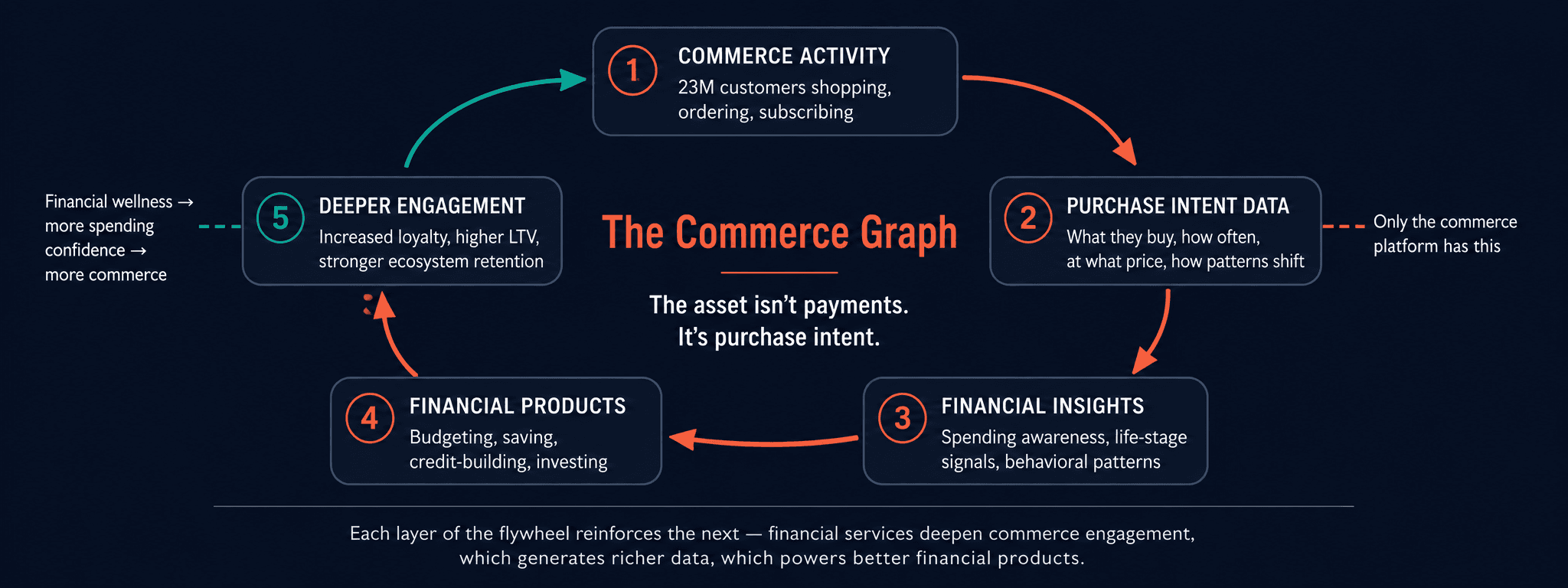

Coupang is the only major player entering from commerce rather than messaging or search. Its 23M-customer commerce graph — what people buy, how often, at what price, and how that shifts over time — could be the foundation for financial products that feel native to how Koreans already spend.

A thesis, not a roadmap. The case maps the landscape, names the risks (breadth vs. depth, trust, regulatory speed), and lays out a 90-day plan to validate which opportunities across payments, asset management, and financial accessibility carry the strongest signal.

Major Players

In Korean FinTech

South Korea’s fintech market is among the most competitive and sophisticated in the world. Three platforms built dominant positions the same way — by starting from communication or search, then expanding into finance.

Each converted an existing daily relationship — transfers, messaging, search — into a financial one. The common move: own the payment, then earn the right to offer everything else.

But the market isn’t static

Three converging forces are reshaping the landscape — and each one favors a new entrant.

New payment rails

Korea’s is expected to enable won-denominated issuance — potentially the largest infrastructure shift in Korean payments since the move from cash to cards. Toss, Kakao, Naver, and Coupang are all positioning for it.

Regulatory interoperability

In January 2025 the Financial Services Commission issued a unified national QR-code standard, mandating compatibility across Kakao Pay, Naver Pay, Toss, and card issuers. Regulators are deliberately lowering ecosystem lock-in — which favors new entrants.

maturation

The playbook for building financial services inside a commerce platform is now proven globally — Mercado Pago, Shopify Capital, SoFi’s productivity loop. The tooling, partnerships, and regulatory frameworks are far more developed than when Toss started from scratch.

All three incumbents started from communication or search and expanded into finance. None of them started from commerce.

An honest assessment

Coupang enters the fintech conversation from a position of commerce dominance and financial-product absence. Understanding both sides of that equation is the first job of any PM taking on this role.

What Coupang brings

- 23 million active customers — nearly half of South Korea’s population

- The deepest commerce data in the country: purchase history, delivery patterns, spending categories, price sensitivity, brand and seasonal behavior, life-stage signals

- Coupang Pay — a 2020 subsidiary with OneTouch Payment (password- and biometric-free checkout via proprietary fraud detection) and ~10M registered users

- Rocket WOW membership (~$4.90/mo) — a recurring relationship across shopping, Eats, and Play

- A WOW co-branded credit card and services

- A growing third-party marketplace — $5.6B in merchant-services revenue in 2024

- An active stablecoin legal buildout and a partnership with Stripe’s Tempo blockchain — infrastructure-level ambition

What Coupang doesn’t have

- A standalone financial product outside the shopping flow

- General-purpose wallet adoption — Coupang Pay is used for Coupang, not daily financial life

- Banking, investing, lending, insurance, or budgeting products

- A financial brand identity separate from “where I order things”

- Profitability in its Developing Offerings segment — still −$168M adjusted EBITDA

The question isn’t whether Coupang should build a fintech product — the company has already committed to that. The question is how to enter a market where three players have multi-year head starts, in a way that’s defensible and native to what Coupang already is.

The wallet war is over. The spending intelligence war hasn’t started.

Coupang missed the first wallet wave in Korea. Toss, Kakao Pay, and Naver Pay won that fight, and they won it years ago. Building “Toss, but inside Coupang” — a general-purpose financial super-app — means playing their game on their turf with a late start. That’s not a strategy. That’s a concession.

But the market is being reshuffled. Stablecoin infrastructure is rewriting payment rails. Regulatory mandates are lowering ecosystem lock-in. Embedded-finance playbooks have matured globally. Every time the infrastructure resets, the advantages built on the old stack become less durable.

And Coupang has something none of the wallet-first players have: the deepest commerce graph in Korea.

Toss knows your bank balance. Kakao Pay knows your payment history. Naver Pay knows your search-to-purchase path. But only Coupang knows what you bought, how often, at what price, in what combination, and how those patterns shift over time. It sees when someone starts buying baby products — a life-stage shift. When someone moves from budget to premium brands — an income shift. When order frequency drops — a possible stress signal, or the first sign of churn.

That data is the foundation for a fundamentally different kind of financial product — one that doesn’t start from the wallet and work toward commerce, but starts from commerce and works toward financial wellness.

The SoFi parallel — and where it breaks

SoFi’s is instructive but doesn’t map cleanly. Each SoFi product — checking, savings, investing, lending — creates a reason to adopt the next. The entry point varies; the loop pulls people deeper. It works because SoFi is a financial company. Every product reinforces the same brand promise.

Coupang is a commerce company. Its version of the loop starts from spending and extends outward — and the financial layer must strengthen the commerce relationship, not replace it. That’s the integration discipline: fintech that deepens engagement with the Coupang ecosystem, not fintech that competes with it.

What this reframe doesn’t answer

This is a thesis, not a roadmap. It argues for an entry angle, not a product spec. The questions that would validate or invalidate it — and shape what gets built first — are what a PM would investigate in the first 90 days.

The right questions in the right order

A PM stepping into this role wouldn’t start with a product spec. They’d start with investigation — validating which opportunities have the strongest signal through user research, data analysis, and stakeholder interviews. Here are the questions I’d prioritize, organized around the three domains the role addresses.

Extending the rail Coupang already owns

Where does Coupang Pay’s OneTouch system have room to extend across the ecosystem — Eats, Play, marketplace merchants — and which friction points represent the highest-impact opportunities?

What does the stablecoin timeline look like under the Digital Asset Basic Act, and how does it change the build-vs-partner calculus for next-generation rails? The Stripe Tempo partnership and active stablecoin hiring suggest this is already in motion — the PM question is sequencing.

What partnership opportunities exist at the device level — Samsung Pay, LG ecosystem embedding — to extend Coupang’s financial presence beyond the app into the physical layer of daily life?

Turning a commerce subscription into a wellness membership

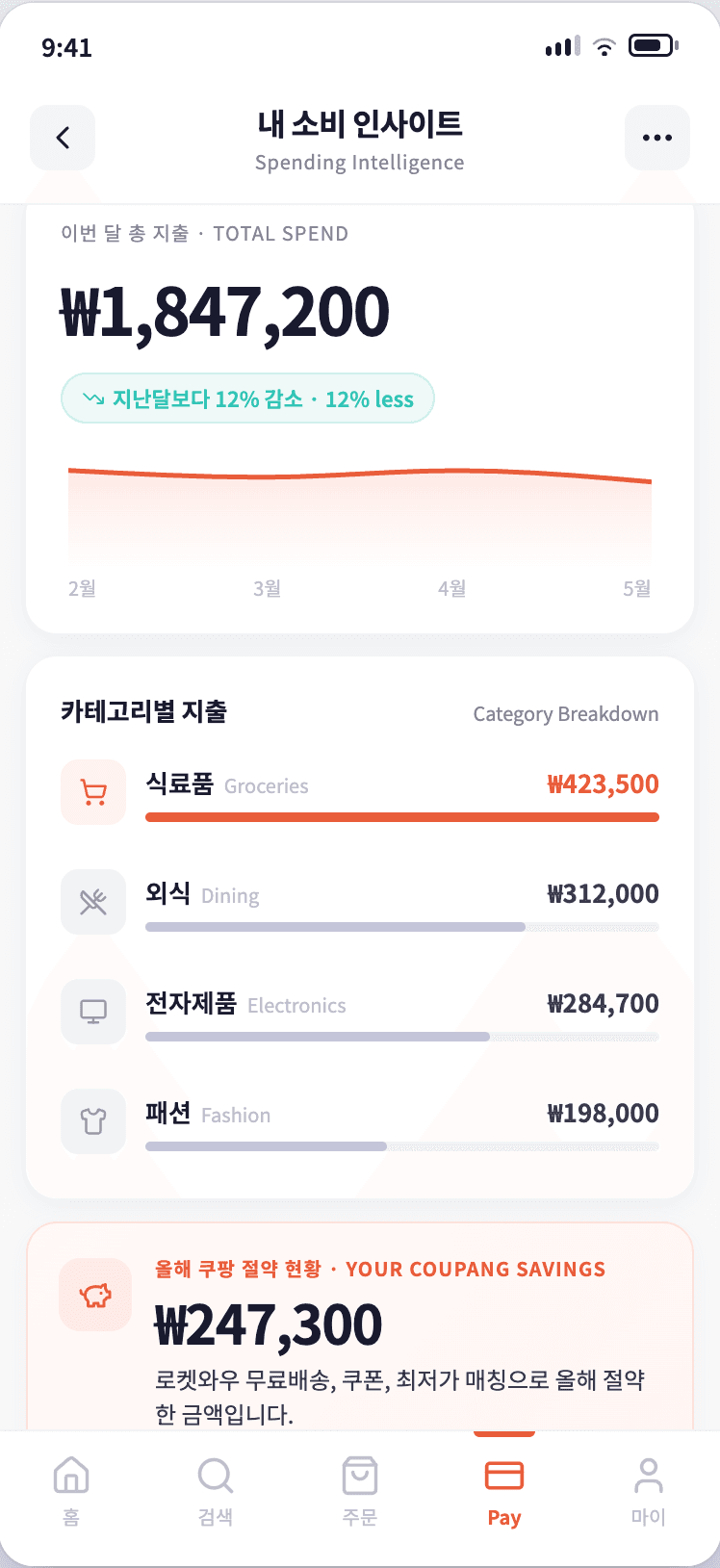

What does Coupang’s commerce data reveal about customer financial life stages, and could purchase-pattern shifts signal the right moments to introduce financial products?

How could micro-investing or automated savings connect to existing Rocket WOW behavior — turning a commerce subscription into a financial-wellness membership?

Pension reform (contributions rising 9% → 13% through 2033) and the corporate retirement crisis (2.35% average returns) create appetite for supplemental tools. What role could a commerce-embedded savings product play in that gap?

Education before credit, by design

How many of Coupang’s 23M customers are among Korea’s ~13M , and could purchase and payment history serve as an alternative credit signal?

What does financial education look like embedded where people actually spend — not a standalone course, but contextual awareness: insights after purchases, savings suggestions at natural decision points?

How do you build financial products like these without cannibalizing revenue — where better spending education actually deepens loyalty rather than dampening it? Put differently: how can improving customers’ financial literacy make Coupang their first stop for all their shopping, increasing both loyalty and spend within the ecosystem?

The integration test

How do these three domains integrate so each one strengthens the others and deepens the commerce relationship — rather than creating three disconnected financial features bolted onto a shopping app?

Both sides of the platform, and beyond one market

Coupang’s third-party marketplace ($5.6B in merchant-services revenue, 2024) is its fastest-growing segment. Merchant-side financial services — working capital, cash-flow tools, seller analytics — would be a second-phase opportunity, but scoping it early informs architecture. Similarly, the role calls for global expansion and localization strategy. Coupang operates in Taiwan, acquired Farfetch (190+ countries), and is entering Southeast Asia. Any fintech architecture needs to account for multi-market deployment from day one.

Market immersion & stakeholder mapping

Landscape, regulatory state, internal partners. Where the signal already lives.

User research & data analysis

Commerce-graph deep dive, life-stage signals, thin-filer sizing, qualitative interviews.

Synthesis & strategic recommendations

Sequenced entry thesis, build-vs-partner architecture, first-product candidate.

Three things that could go wrong

Opportunity analysis is easy. Risk analysis is what separates strategy from wishful thinking. Any PM building this product would need to navigate three persistent tensions.

Breadth vs. Depth

The temptation to build a full financial super-app on day one is real — especially when competitors already offer 70+ products. But Toss took nearly a decade to get there, and they started from a single killer feature: free transfers. Coupang doesn’t have a decade, but it also can’t ship everything at once without quality degradation. The discipline is to start narrow, prove the commerce-to-finance bridge creates genuine value, and expand only after earning the right. The willingness to give up what you want to do in order to win what you must isn’t a management principle here. It’s a survival requirement.

Ecosystem integration vs. Brand risk

Financial services inside the ecosystem could deepen loyalty and lift lifetime value. But financial products carry a different trust burden than commerce. A late delivery is frustrating. A financial failure — a breach, a poorly designed lending product, a confusing fee — can be relationship-ending. Coupang faced political backlash after a data incident in 2025. In financial services the stakes for trust are higher still. The product needs to be right before it’s fast.

Regulatory complexity vs. Speed-to-market

Korean fintech regulation is sophisticated and moving fast — stablecoin legislation pending, pension reform underway, the tightening household lending, new interoperability mandates. Moving quickly is a Coupang value, and it should be. But financial products require licensing, compliance infrastructure, and regulatory relationships that can’t be rushed. Each domain’s build-vs-partner-vs-acquire decision is fundamentally a speed-vs-control tradeoff. Getting the architecture right early prevents costly restructuring later.

A bridge perspective

This case study was built on publicly available research. But it reflects a specific orientation.

I’m drawn to problems that sit at the intersection of strategy, customer behavior, technology, and trust — where the work isn’t shipping a feature but sequencing bets under real ambiguity. A fintech product inside a commerce ecosystem is exactly that: a customer-insight problem, a data problem, a UX problem, and a trust problem at once.

Fifteen years building technology products across development, architecture, design, and UX — including regulated environments where compliance, user trust, and stakeholder alignment are daily concerns. An MBA that sharpened strategic and financial analysis. And Korean family heritage that provides not expertise, but something more useful for this role: a bridge.

Coupang is a culturally hybrid company — NYSE-listed, Korean American-founded, Seoul-headquartered, globally expanding. The Senior PM for its new fintech product needs to operate across those boundaries. The Korean market deserves deep respect and genuine curiosity, not assumptions. Cultural fluency is earned through immersion, user research, and relationships — not inherited. But the cross-market lens the global-expansion mandate requires — thinking simultaneously about Seoul and Taipei and beyond — is where a bridge perspective creates distinct value.

The quality of thinking and clarity of communication in this case study reflect what stakeholder briefings, product reviews, and cross-functional alignment would look like in the role. If it earned your attention this far, that’s the case being made.

Ask about the case.

Test the thesis, push back on the sequencing, or ask how the bridge perspective shows up in practice. The chat below is wired to my portfolio AI — standard for now, with a case-specific extension on the way.

I’m an AI built on James’s thinking behind this Coupang fintech case study. Ask anything about the reframe, the 90-day plan, or the tensions worth naming — or pick a question below.

Experimental AI trained on James’s portfolio. Responses are general — not affiliated with or endorsed by Coupang.

✓ The questions are defined. ✓ The risks are named. ○ The conversation about answers is not.

Only 11% feel ready for what’s coming. The questions are clear. The window is open. What comes next is the conversation about answers.